Key Takeaways:

- The Federal Open Market Committee (FOMC) is proceeding carefully, something we highlighted here almost a month ago.

- Geopolitical tensions post key risks to the outlook, something that could ensure the Federal Reserve (Fed) takes a wait-and-see approach with further tightening.

- Additional hikes are in the cards only if there is additional evidence of a strong economy.

- The Fed is not yet convinced where inflation will settle over the next few quarters, which means the committee will not pre-commit. Each meeting will be a live meeting.

The Bottom Line

As of last Friday, markets were pricing in a roughly 20% chance the Fed will increase rates in December, and if not in December, then a higher likelihood of an increase in January. However, we believe the economy is slowing enough that the markets are overpricing the likelihood of more rate hikes.

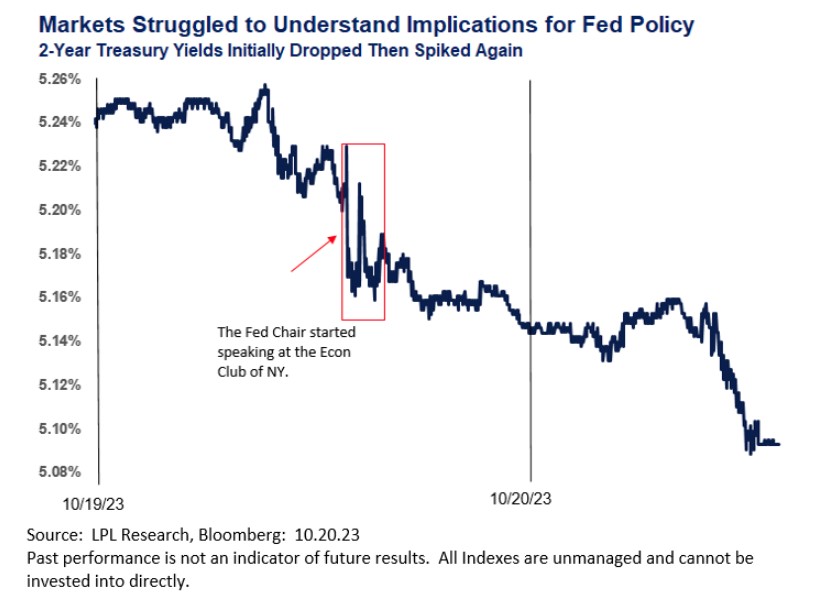

Fed Chairman Jerome Powell addressed the Economic Club of New York yesterday along with a brief—and unscheduled—presentation from a group aptly named Climate Defiance.[1] Despite the interruption, the Chair was going to continue with the theme developed earlier in the week from several other members of the FOMC. To wit, the Committee sees risks as roughly balanced between over- and under-tightening. If rates were too low, inflation could resurge and if rates get too high, the economy were more likely feel a hard landing. In an effort to calm markets, Powell reiterated his desire for the FOMC to proceed carefully in the next several months.

But, markets initially did not know how to process his comments. Yields on the 2-year Treasury initially dropped on the news and then reversed course only to dip several basis points again. (One basis point is 0.01%.) Markets eventually were able to process the new information and yields continue to fall as of Friday morning, October 20th, 2023.

Is Inflation Easing or Not?

The temporary scare for markets was the confession that the FOMC is unsure where inflation will settle over the next few quarters. In our view, many aspects of inflation are getting less sticky, creating reasonable expectations that inflation will ease further in coming months. Rent prices are off their peak according to industry reports, and investors should also know there is a sizable lag in time between a reported movement in industry rental data and the official government metrics. By the end of the year, the inflation trajectory should be clearer for both policy makers and investors.

Recession or No?

From an investment standpoint, the “recession call” may end up being less relevant. A recession could still emerge as consumers buckle under debt burdens and use up their excess savings, but a Fed sensitive to risk management might provide the salve necessary for more risk appetite. Investing is a relative game, meaning the U.S. could experience the 3 D’s of an economic contraction—depth, diffusion, and duration—but at the same time, still outperform other markets and hence, still be an attractive option for investors looking for calculated risk.

A shallow recession would likely provide a boon for the domestic markets, as it would increase the odds of the Fed cutting rates and bring the labor market into better balance. History shows markets tend to rally as the Fed pivots away from a tightening bias.

Recent Asset Allocation Change

The Strategic and Tactical Asset Allocation Committee (STAAC) recently recommended reducing allocations to developed international equities and increasing allocations to the U.S. Growth estimates for Q3 will be released October 26 and will likely be better than expected in the U.S. and deteriorating technical analysis trends in Europe are the primary reasons for the change, while currency risk is elevated.

Conclusion:

Markets struggled to process Chairman Powell’s remarks yesterday. However, investors should take yesterday’s speech in the context of what they learned from the latest Beige Book in order to get a clearer picture on future interest rates. Investors learned earlier this week that business is slowing and delinquencies are picking up, indicating the economy is no longer on a strong growth trajectory. By the end of the year, markets will get a clearer view and policymakers will likely have more clarity on growth and inflation trajectories. Patience is a necessary trait for long-term investors.

IMPORTANT DISCLOSURES

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors. To determine which investment(s) may be appropriate for you, please consult your financial professional prior to investing.

Investing involves risks including possible loss of principal. No investment strategy or risk management technique can guarantee return or eliminate risk in all market environments. For more information on the risks associated with the strategies and product types discussed please visit https://lplresearch.com/Risks

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and do not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

Unless otherwise stated LPL Financial and the third party persons and firms mentioned are not affiliates of each other and make no representation with respect to each other. Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services.

All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

Securities and advisory services offered through LPL Financial, a registered investment advisor and broker-dealer. Member FINRA/SIPC.

Tracking # 494454

[1] https://www.barrons.com/livecoverage/fed-jerome-powell-speech-today/card/protesters-interrupt-powell-speech-VclauoymYfBimWMxblcn